What does this mean?

In economic theory, we distinguish between different types of markets and, following Heinrich von Stackelberg's market form scheme, can generally classify them into nine market forms based on the number of market participants (i.e., suppliers and buyers). The three most important market forms are monopoly, oligopoly, and polypoly.

To understand the processes in the different market forms, let's look back at the beginning:

A market always arises where supply equals demand and, in economics, generally refers to the place where supply and demand meet. When supply and demand for a particular good are equal, we speak of market equilibrium, which is characterized by the equilibrium price and the equilibrium quantity. The price is therefore determined by the supply and demand.

Difference between the 3 main Market Forms:

Table of Contents

Polypoly:

In a polypoly, many suppliers face many buyers. Each supplier has only a relatively small market share in the market, which is why individual decisions cannot influence market developments. All suppliers in a polypoly are therefore price takers or quantity adjusters. Individual firms consider the market price as given, and their only remaining action parameter is the output quantity. In a polypoly, perfect competition prevails, i.e., the following assumptions are made:

The only remaining action parameter is the output quantity. In a polypoly, perfect competition prevails, i.e., the following assumptions are made:

- Homogeneous goods are offered

- Perfect information prevails

- All market participants react infinitely quickly to changes

- No barriers to market entry

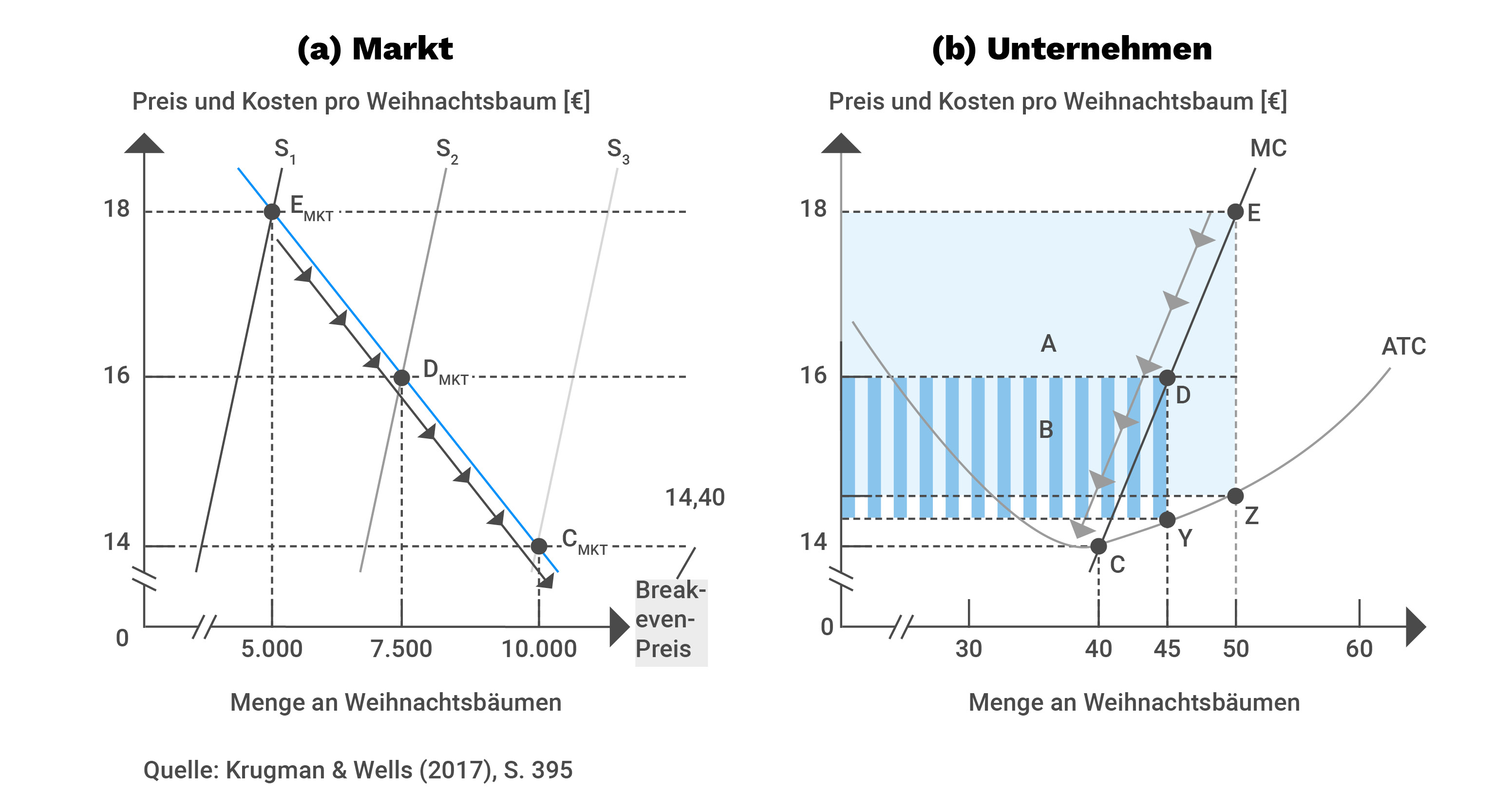

Because there are no barriers to market entry, firms can enter and exit the market at any time. Point EMKT in the figure shows the original short-term market equilibrium. If the market price is high and firms are generating an economic profit, new firms will enter the market. This shifts the short-term supply curve to the right (Figure 1: from S1 to S2), because profit always leads to a larger quantity being produced. A new short-term equilibrium is established (point DMKT). Now the market price is lower, but total production is higher. Accordingly, the profits of existing firms also decrease, but profit still remains (rectangle labeled B).

Further market entries shift the short-term market supply curve further to the right (S3), the price continues to fall, and the industry's output continues to increase. New firms now come to a halt when marginal costs equal average total costs (point C). The market price is now at the break-even point, meaning that the firms operating in the market achieve zero economic profit and there is no incentive to enter or exit the market. We are in equilibrium, which describes the long-term market equilibrium (point CMKT). If the market price continues to fall, market exit occurs.

In perfect competition (polypoly), marginal revenue equals market price because firms are price takers. Therefore, the condition for profit maximization is: market price/marginal revenue = marginal cost.

Monopoly:

In a monopoly, a single supplier faces all demand (many buyers). The products offered are not differentiated but homogeneous.

The following five barriers to entry are distinguished:

- Sole ownership of a scarce or crucial resource

- Increasing returns to scale

- External growth

- Network externalities

- State-created monopolies

Increasing returns to scale are understood as falling average total costs and rising production volumes, which ultimately lead to a natural monopoly. External growth refers to the merger of companies. In contrast, competition law regulates this today to prevent the formation of monopolies.

Natural monopolies arise when average total costs fall above the relevant range of production volumes. This creates a barrier to entry because an existing monopolist has lower average total costs than any company wishing to enter the market.

A monopolist only needs to consider the response of aggregate demand when making its supply decision. Because the monopolist is the sole supplier in the market, he can pursue either an active price or quantity policy in his supply decision. However, both are not possible. If he decides to pursue a price policy, he sets a fixed price per quantity. Consumers can then decide how much to purchase from the monopolist. With quantity policy, it is exactly the other way around. Here, the monopolist determines the quantity to be purchased and the consumer determines the price. The monopolist does not have to consider competitors in his decisions. This phenomenon is also referred to as autonomous pricing behavior or autonomous quantity fixing.

In a monopoly, a further distinction is made between limited and bilateral monopolies. In a limited monopoly, an actor faces a few market participants on the opposite side of the market. An example of this is the market for armaments. The state, as the sole buyer, faces several armaments companies. The monopolist's power is limited here by other suppliers.

In a bilateral monopoly, on the other hand, the supply and demand power are at their lowest. Here, suppliers and buyers mutually control each other's power. The labor market would be a suitable example.

The special feature of a monopoly is that it allows for long-term economic profits. Profit maximization in a monopoly occurs where marginal cost equals marginal revenue. This is where the optimal production quantity lies. The reason for the deviation from the monopoly at the profit-maximizing production level is its demand curve. It corresponds to the market demand curve, since it is the only supplier in the market. Due to the characteristic downward slope of the demand curve, the price of the good no longer corresponds to marginal revenue. The marginal revenue curve lies below the demand curve here. Due to the price effect, the higher the quantity, the lower the price. An increase in production by the monopolist has two opposing effects. First, the quantity effect, because total revenue increases by the price at which the additional unit is sold, and second, the price effect. In order to sell the last unit, the monopolist must lower the market price for all units sold. This reduces total revenue.

To maximize profits, a monopolist will therefore offer where marginal costs equal marginal revenue. Marginal revenue is always below price.

Oligopoly:

In an oligopoly, a small number of suppliers face the entire demand. No supplier holds a monopoly, but each company can influence the market price. This market structure is very common in consumer goods markets. For example, the detergent market is dominated by a few large suppliers. In contrast to a monopoly, oligopolistic suppliers must consider not only the reaction of consumers but also the reaction of competitors. Because in an oligopoly each supplier has a relatively large market share, the decision of another oligopolist affects their own market position. This is called an action-reaction alliance, which requires strategic competitive behavior. Competitors act interdependently: The action of one supplier triggers a reaction from the other suppliers.

The existing interdependencies between suppliers in the market are therefore of great importance in an oligopoly. Strategic behavior plays a central role here. If oligopolists join forces and act together like a monopolist, they can jointly maximize their profits. The incentive to form what is known as a cartel is strong, but is prohibited in Germany. On the other hand, every company also has an incentive to violate cartel rules in order to potentially further maximize profits. Oligopolists can therefore make their decisions either simultaneously (so-called collusion) or sequentially.

The prisoner's dilemma from game theory illustrates the situation of oligopolists: The prisoner's dilemma represents a modeled situation of two prisoners who are accused of having committed a crime together and are interrogated individually. Both prisoners cannot communicate with each other. The following situation arises: If both deny the crime, both receive a low sentence because very little can be proven against them. If both confess, both receive a high sentence, but not the maximum sentence because of their confession. If only one of the two confesses, they go unpunished, while the other prisoner, as the convicted and non-confessed offender, receives the maximum sentence. The dilemma here is that each prisoner must make a decision without knowing the other prisoner's decision. The final sentence is no longer in the hands of one prisoner, but also depends on the decision of the other. Both decisions must be considered. The dominant strategy of both prisoners would be to confess, which is also known as a Nash equilibrium or non-cooperative equilibrium. In this case, the effects of this action on the outcome received by the other prisoner are ignored. However, cooperation between both prisoners would lead to a lower sentence and thus also to a lower overall sentence.

In oligopoly markets, we find numerous variants of oligopolistic interactions. In addition to an oligopoly with homogeneous goods, heterogeneous oligopolies with differentiated products play a major role in reality. Action parameters include prices, quantities, advertising, and product innovation. Thus, there are a large number of oligopoly models.